Nvidia(Nasdaq: NVDA) became the child of the poster for the rise of artificial intelligence (AI) at the beginning of 2023. The chips of the data center used to train and exploit powerful models of AI created a rapid growth market that Nvidia has mainly dominated. But just like the Internet in the late 1990s, excitement and novelty can sometimes let the media to become a little too far before reality.

Recently, the markets began to let out hot air. THE Nasdaq Composite is almost 10% reduction on its top, flirt with, technically, a correction. Nvidia’s shares have decreased by almost 25% since their summit in early January.

It can be frightening when the equity prices drop like that, but I am here to warn investors to let sales go too far. The NVIDIA DIP has undoubtedly created an opportunity to purchase for long -term investors. I broke out why and how to take advantage of it below.

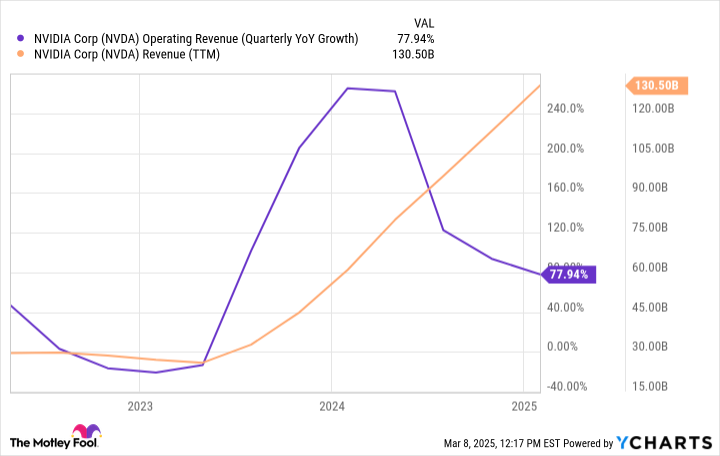

As the internet in the late 1990s, the media threshing behind a new technology could create a bubble. Some internet actions exploded above before crashing when music (media threshing) stopped. This could very well happen with certain AI stocks. However, Nvidia is probably not part of it. Nvidia’s actions have greatly appreciated in the past two years, but real business growth has brought the stock, not the media threw. Nvidia has generated $ 130 billion in revenues in the last four quarters and still increases to almost 80%:

This trend does not stop; The main technological companies investing in AI data centers, also called AI hyperscalers, reported continuous investments in 2025. The reports indicated by IA expenses could exceed $ 320 billion this year. Which comes in the heels of AI hyperscalers, like Alphabet And MicrosoftNoting in their most recent income than cloud demand for AI continues to exceed the available cloud capacity. OPENAI, one of the main IA developers and Chatgpt creator, recently said that he was short of GPU chips, delaying product deployments.

It seems that the growth of Nvidia AI is authentic and remains heated to red. It is not a bubble, not when the shares are negotiated with a price / benefit / benefit ratio (p / e) of 38, but analysts think that profit per share will increase more than 50% this year and will increase an average of 34% per year in the long term.

There is nothing like a risk without risk. The risk for Nvidia is that the Small handful of companies Investing all this money in AI is starting to shop elsewhere or fully close their wallets. This may be why NVIDIA’s evaluation is so cheap compared to its expected growth in profits.

Although you can respect the risks (this is why you diversify your wallet), there is evidence that Nvidia can prosper beyond a temporary investment cycle of the AI data center.

The opportunity in a generative AI extends beyond models such as chatgpt to other applications, including autonomous vehicles, humanoid robotics and agentic AI that replaces humans in call centers. It also goes beyond business level. As technology progresses and costs decrease, the development of AI will pass downstream in small businesses, even individuals. NVIDIA recently announced a SuperCalculator powered by Blackwell that adapts to an office.

Access to AI innovation can extend far beyond today’s AI hyperscales. Nvidia has an interior track to monetize it as long as the company can build an ecosystem around its domination in accelerator fleas.

NVIDIA continues to provide stellar commercial results. Until it changes, it is difficult to doubt the position of the most important technology (AI) of this generation. Even if Nvidia has increased the 19% profits per year in the long term, half of what analysts currently estimate, the current P / E ratio of action is equivalent to a price / benefit / growth / growth ratio (PEG) of around 2, a reasonable price for this growth. In other words, Nvidia offers a safety margin if things are not going as well as hope in the coming years.

At the same time, equity prices can fluctuate with market volatility and economic and geopolitical changes. The past few weeks have shown it. Nvidia has decreased by almost 25%, which could continue if wider market turbulence continue.

While Nvidia has a solid argument as a mass of AI to buy now, investors should always move slowly. Consider the average cost in dollars, buying a little at a time to capture the additional value if prices are headed even more. Remember that you will see the prices drop, unless you perfectly timed the bottom, which almost no one does.

Thinking about the next decade, it is difficult not to like NVIDIA’s combination of future advantage and current value.

Before buying actions in Nvidia, consider this:

THE Motley Fool Stock Advisor The team of analysts has just identified what they believe 10 Best Actions So that investors are buying now … and Nvidia was not part of it. The 10 actions that cut could produce monster yields in the coming years.

Inquire Nvidia Make this list on April 15, 2005 … if you have invested $ 1,000 at the time of our recommendation, You would have $ 690,624! *

Now it’s worth notingStock advisorTotal average yield is821% – an outperformance of marking compared to the market compared to167%For the S&P 500. Do not miss the last list of the best 10, available when you joinStock advisor.

Suzanne Frey, director of Alphabet, is a member of the board of directors of Motley Fool’s. Justin Pope Has no position in the actions mentioned. The Motley Fool has positions and recommends Alphabet, Microsoft and Nvidia. The Motley Fool recommends the following options: Long January 2026 Calls $ 395 on Microsoft and Court January 2026 405 $ calls Microsoft. The Word’s madman has a Disclosure policy.

Stocks to Buy Right Now?")