For the past two years, technological actions have been swinging thanks to an extremely optimistic story surrounding artificial intelligence (AI). Among the biggest AI winners, software companies were a theme that I do not see changing anytime soon.

Below, I will compare two of the biggest names in company software benefiting from the AI revolution: PALANTOUT Technologies(Nasdaq: PLTr) And Dirty(NYSE: CRM). While everyone seems to be well positioned to continue to overcome the wave of AI, I see palanting as the higher choice for growing investors.

Let us make the way in which each of these software leaders affects the AI sector and evaluates why I think Palantir will become the biggest company by the end of the year.

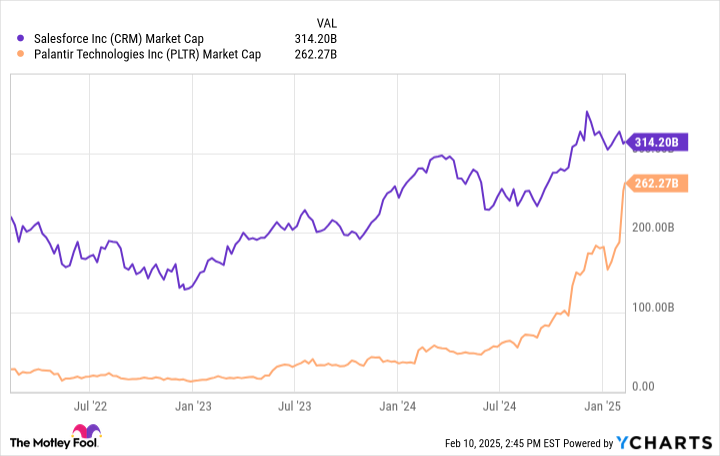

To date (February 10), Salesforce has a greater market capitalization than a palantant of around 52 billion dollars. That said, the underlying trends shown in the table below are quite interesting.

Consult the difference between how the assessment of each company has evolved since AI has become the next megaTend. Over the past two years, Palantir’s assessment has developed considerably. On the other hand, the Salesforce price movement has shown much more flows and flows. Consequently, there is a clear convergence in the graph below with the market value of Palantir which begins to encroach on that of Salesforce.

Salesforce has a number of properties, including data analysis platform table and the Slack messaging tool. The previous strategy of the company consisting in acquiring competing companies and integrating them into the main ecosystem has helped create a software suite that offers companies a variety of data -oriented applications, but investors finally got tired of such an approach.

In the past two years, Salesforce has been under a meticulous examination of Wall Street to start providing an acceleration of income and expansion of more robust beneficiary margins to exclusion Inorganic assets purchased by acquisitions.

I admit that Salesforce made this promise … for the most part. The problem that Salesforce continues to face revolves around consistency. In other words, the company sometimes blows expectations of Wall Street out of the water, while at other times, investors scratch their heads wondering what is happening during the execution.

For this reason, I am not fully sold that Salesforce will dominate his pocket in the AI domain. More specifically, the most recent area of interest of the company, called Ai -Ai, faces fierce competition – namely MicrosoftA much larger company with a stronger assessment.

When you add that Salesforce faces a number of tangential competitors, including Monday.com,, Hubspot,, Atlassian,, Asana,, Working dayAnd more, I find it difficult to see how he sails in the middle of all these companies.

On the other hand, Palantir – which is much smaller than Salesforce in income and income – is associated with Microsoft, Meta-platforms,, AmazonAnd Oracle. For me, Big Tech’s decision to work alongside Palantir rather than launching competing products represents enormous potential since the company continues to develop its greatest growth engine, the continuation of artificial intelligence platform software (AIP).

Image source: Getty Images.

The graph below illustrates consensus estimates among Wall Street analysts for income growth and profits by action (BPA) between Salesforce and Palantir.

The dichotomy shown above is obvious: Wall Street estimates much less acceleration of income and profits from Salesforce from Palantant in the next two years. My interpretation of these forecasts is that analysts can see more competitive winds for Salesforce compared to Palantir.

To be fair, it should expect a certain measure. Salesforce is a much larger company than Palantir, and therefore at some point, the business growth profile will mature.

However, I have not entirely adhered to this idea because AI is supposed to represent transformative opportunities for companies of all sizes. Given the banal growth profile for Salesforce, I wonder if Wall Street shares my suspicions that AI may not have such an influential influence for the company as for other software companies, such as Palantant.

For these reasons, I would not be surprised to continue attending incoherent trends in Salesforce throughout this year (and maybe even more). On the other hand, The prospects for palantir seem strong, And I think investors could continue to applaud the stock – propel its valuation even higher in 2025.

I think there could be a certain contraction in the market capitalization of Salesforce and even more expansion at Palantir, thus respecting the gap between the two companies even more. If that happens, I think Palantir will emerge as the most precious company by the end of the year.

Have you ever had the impression of having missed the boat to buy the most successful actions? So you will want to hear this.

On rare occasions, our team of analysts experts issues a The “Double Down” stock Recommendation for the companies they think are about to burst. If you are afraid, you have already missed your chance to invest, it’s the best time to buy before it is too late. And the figures speak for themselves:

NVIDIA:If you have invested $ 1,000 when we doubled in 2009,You would have $ 360,040! *

Apple: If you have invested $ 1,000 when we doubled in 2008, You would have $ 46,374! *

Netflix: If you have invested $ 1,000 when we doubled in 2004, You would have $ 570,894! *

Currently, we are issuing “double” alerts for three incredible companies, and there may be no luck like this as soon as it is.

Randi Zuckerberg, former Director of Development of the Facebook and Sister of the CEO of Meta Platforms, Mark Zuckerberg, is a member of the board of directors of Motley Fool’s. John Mackey, former CEO of Whole Foods Market, a subsidiary of Amazon, is a member of the board of directors of Motley Fool’s. Adam Spatacco has positions in Amazon, Meta Platforms, Microsoft and Palant Technologies. The Motley Fool has positions and recommends Amazon, Atlassian, Hubspot, Meta Platforms, Microsoft, Monday.com, Oracle, Palantant Technologies, Salesforce and Workday. The Motley Fool recommends Asana and recommends the following options: Long January 2026 Calls $ 395 on Microsoft and Court January 2026 405 $ calls Microsoft. The Word’s madman has a Disclosure policy.